The MP Curve and Monetary Policy

Econ 105C

- Federal Funds Market

- How the Fed Controls Interest Rates

- Targeting Interest Rates vs. Targeting Money

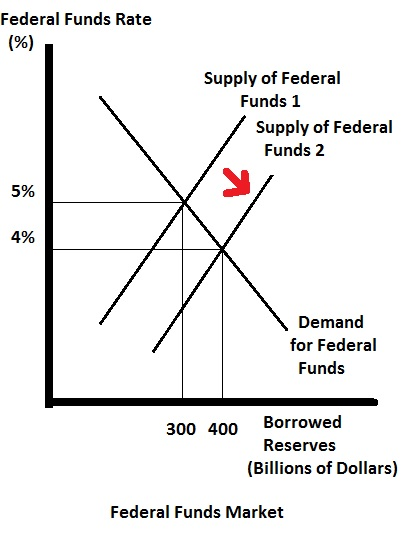

Federal Funds Market

- Banks hold reserves in cash and at the Fed

- Reserves held at the Fed are known as “federal funds” and are like electronic cash

- Federal funds are very liquid and can be used as payments, to satisfy reserve requirements, etc.

- Over $2 trillion of interbank payments are made every day

- Banks can borrow federal funds from other banks or from the Fed in order to make payments/satisfy reserve requirements

- These federal funds loans are typically made for one day at a time

- The central bank is a “banker’s bank”; banks can deposit reserves at and borrow from the central bank

- There are three “federal funds” interest rates

- Interest rate banks receive on reserves (IOR rate)

- Interest rate banks pay for loans

- Interest rate banks receive pay each other for federal funds loans

Interest on Reserves (IOR)

- The IOR/IORB rate (Interest on Reserves (Balances)) is the rate that banks receive from the Fed on federal funds

- The IOR rate improves the Fed’s ability to control the R/D ratio, or rr

- This allows the Fed to better control the money multiplier and total amount of money

Discount Rate (Primary Credit Rate)

- The federal funds that the Fed loans out to banks are collateralized so the risk to the Fed is low

- These loans are known as “discount window” loans and the interest rate is known as the discount rate or primary credit rate

- The discount window is rarely used because it is a sign of weakness to take a loan from the Fed

Federal Funds Rate

- Banks can borrow and lend federal funds to each other via the federal funds market

- The interest rate on one-day loans between banks for federal loans is known as the federal funds rate

- The federal funds rate is the one that the Fed targets every day

- In theory, the federal funds rate should be between the IOR and primary credit rate, or else banks would have no incentive to give and receive loans from each other

- If the Fed wants to add reserves to the federal funds market, the Fed buys government bonds from banks

- Banks trade bonds for cash reserves, or federal funds, increasing the federal funds in circulation

- If the Fed wants to sell reserves to the federal funds market, the Fed sells government bonds to banks

- Banks buy bonds for cash reserves, reducing the amount of federal funds in circulation

- Both processes are accomplished through auction to banks

How the Fed Controls Interest Rates

- There are many other short-term interest rates, such as the treasury bill rate, commercial paper rate, bank deposit rate, etc.

-

Arbitrage is the act of buying an asset in one market and selling it in another market at a higher price to make a profit

- If there is a significant profit to be made via arbitrage, then arbitrageurs would being abusing that fact which would drive the prices closer together

- Arbitrage applies to short-term interest rate markets as well

- If other short-term interest rates were different, then financial traders at banks would begin arbitraging away the difference

- For example: if the federal funds rate was 5.4% and the 1-month Treasury bill interest rate was 5.9%, then banks would borrow federal funds and buy Treasury bills to make a profit

- Due to arbitrage, all US short-term interest rates move along with the federal funds rate

- Arbitrage is harder to do between two different assets, so long-term interest rates can differ from short-term interest rates

- This means that the 1-month Treasury rate is very close to the federal funds rate, but the 10-year Treasury rate is less linked to the federal funds rate

Real vs. Nominal Interest Rates

- The IS-MP curve is in terms of real interest rates, but the cental bank can only control the nominal short-term interest rate

- In the short-run, we think of inflation as fixed, so the central bank controls the real interest rate by controlling the nominal interest rate

Targeting Interest Rates vs. Targeting Money

- The quantity theory of money says the central bank should target the quantity and growth rate of money

- MV = PY

- The IS-MP model indicates that the central bank targets the interest rate directly

- Because the demand for cash and reserves varies (sometimes by a lot), the velocity of money is not constant, and the money multiplier can shift substantially, it’s difficult to target a monetary base

- This leads to the Fed targetting a federal funds rate instead due to its stability

- Makes it easier to formulate monetary policy, decide on a interest rate level, and communicate monetary policy

- All of the world’s major central banks use a short-term interest rate target than a monetary base target